Get ready for Single Touch Payroll Phase 2 (note Xero deferral until 31 March 2023)

What exactly is STP Phase 2 and how is it different from phase one?

This is the next stop on the STP journey. Where phase one was a way of reporting employees’ tax and super to the ATO, STP Phase 2 expands the program to capture more information. This will reduce the compliance burden for employers and individuals, and help the admin side of things for social support services – think Centrelink. When you do interact with government services, these changes will make that process easier.

What new information will be included?

Under STP Phase 2, you will be required to report additional information to the ATO under a few new areas. The main ones to be aware of relate to the following:

- Tax file number declaration: Currently, these declarations capture details on employment type (full time, part time or casual) and different tax factors that influence PAYG withholding, like a HELP debt, as well as the TFN itself. This will all be included in your STP report via an automated six-character tax treatment code for each employee and means TFN declarations will no longer need to be sent to the ATO after collection.

- Termination reason: The reason why someone leaves a business will need to be provided in your STP report, such as if it was voluntary or a redundancy. This means no more employee separation certificates.

- Employment basis: Previously optional, it will become mandatory to report an employee’s work type. This includes full-time, part-time or casual, along with new categories like labour hire, volunteer agreement or non-employee.

- Income stream collection: Phase 2 will require employers to break down payments into more detail under a new grouping called income stream collection. This has three main areas:

- Income types: Where before income was classified under one label, in Phase 2 each amount paid to an employee will now be assigned to an income type. These include salary and wages, closely held payees (e.g. family members), working holiday makers, and labour hire, among others.

- Country code: You will have to include a country code for employees who report to tax jurisdictions outside of Australia. This is most relevant for businesses with staff on certain visas (like working holiday) as you will need to provide their home country.

- Disaggregation of gross: Currently, STP reports include a gross (total) amount which is the sum of a number of payment types. This will now be broken into more detail to include: allowances (all must be separate); bonuses and commissions; directors’ fees; overtime; paid leave; salary sacrifice. Paid leave will also be categorised using leave type codes.

- Salary sacrifice: Since these contributions can no longer be used to reduce ordinary earnings or count towards superannuation obligations, they need to be separately reported in STP. You can no longer report the post-sacrificed amount via payroll.

- Lump sum E payments: This is used when you make lump sum payments for back pay from previous income years. Previously, it was shown on a separate line item in an employees’ payment summary. In Phase 2 it must be included in STP reports before finalising an employees’ records. This will remove the need to provide employees with Lump Sum E letters.

What do you need to do now?

Note that Xero has deferral until 31 March 2023 for all customers.

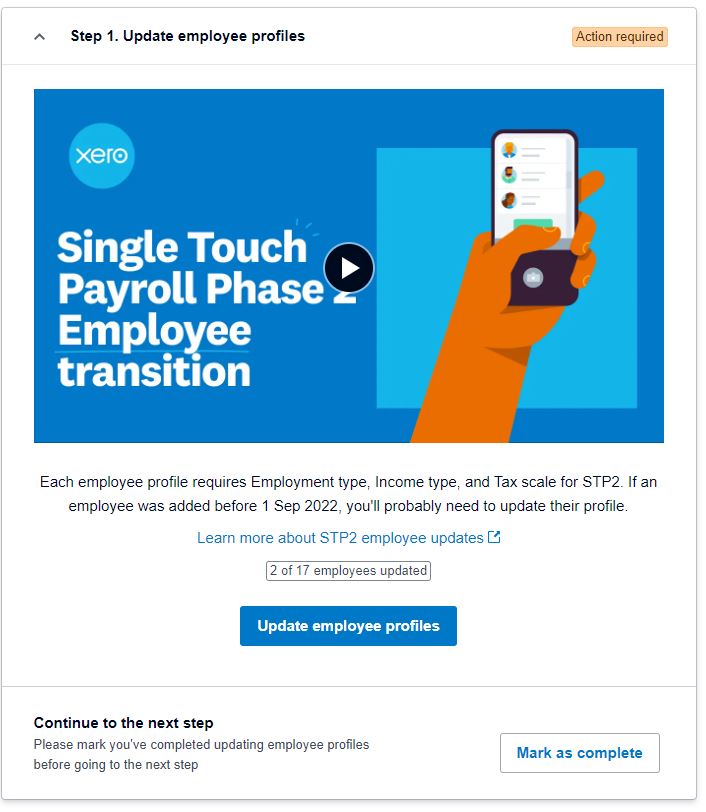

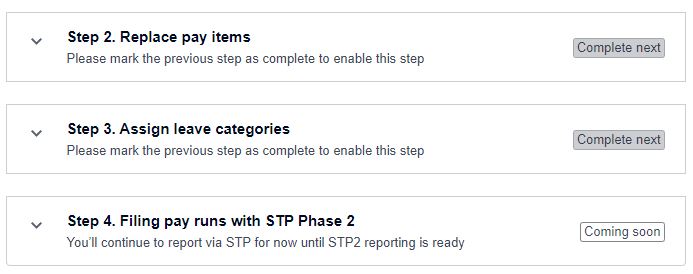

If you want to get ready now, you need to go to Payroll and follow these steps to update the pay items as per below

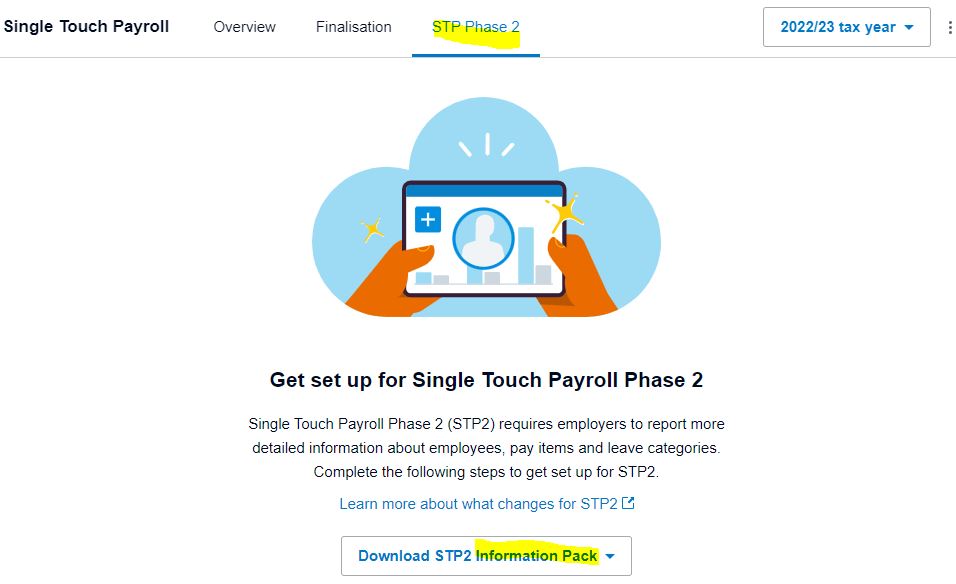

The information pack has details of relevant pay items and changes, with good comparison between STP 1 and STP 2 reporting.